Tag:startup

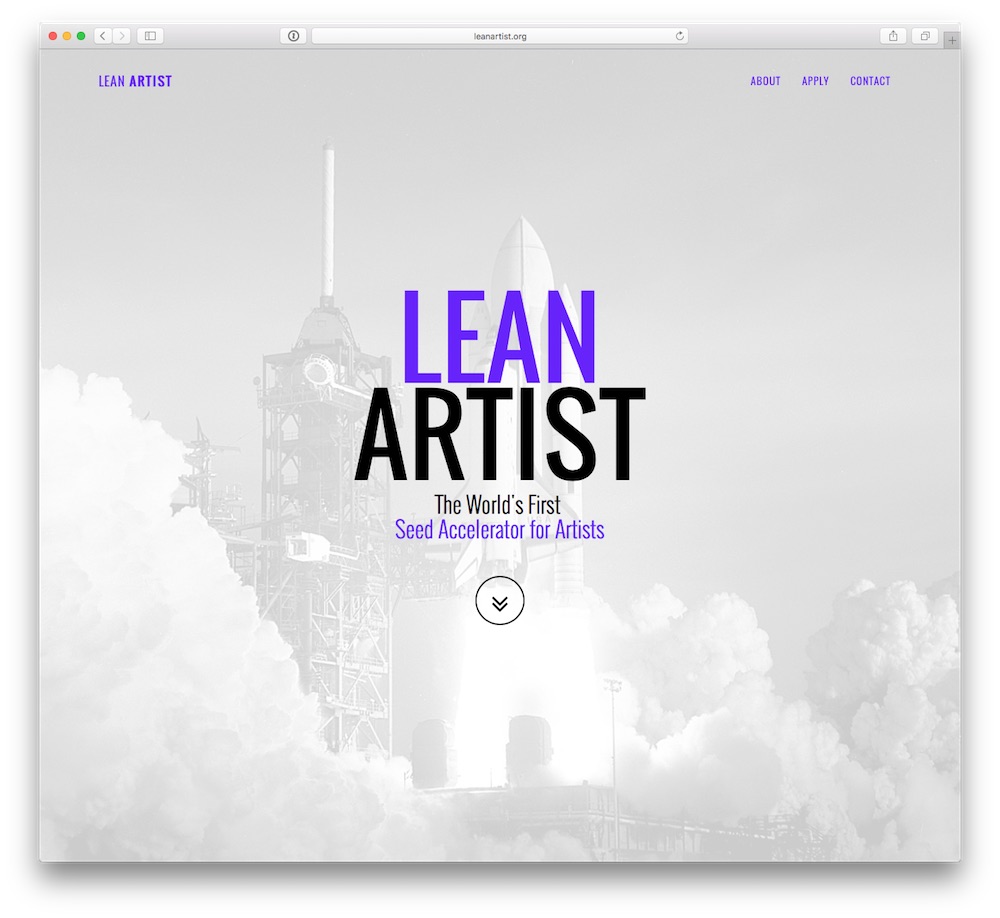

Check out Lean Artist – The World’s First Seed Accelerator For Artists. The Seed Accelerator will invest 3000€ in 10 artists to create culturally disruptive startups. The Accelerator is lead by Toronto based New Media Artist Jeremy Bailey, whose work is on exhibition Tate Liverpool, Transmediale Berlin, and Balice Hertling in Paris among others. The first cohort will start August 26-28 2016 as is part of the A/D/A Hamburg 2016, a conference about future utopias for today’s urban citizen. I was asked to join […]

While being in Sydney in early 2016, I joined a team to create a food delivery startup as part of a Management & Innovation workshop at UNSW Business School in conjunction with Michael Crouch Innovation Centre. I worked on this project part time while conducting research at UNSW into policy towards entrepreneurship and innovation and drafting a policy review of the Tech Startups Action Plan by the City of Sydney. The workshop was organised around the structure of typical startup accelerator programs, working […]

I recently went to Starbucks in Downtown Palo Alto for some Frappuccino to kill some time. While waiting for the hours to pass, surfing the web on my iPhone, I ran out of power quickly. This is when I noticed the Powermat wireless charging stations they offered in the store. This is how it works: “Powermat lets you power your phone without wires or cords or worries. Simply visit one of our Powermat locations. They’re easy to find using our […]

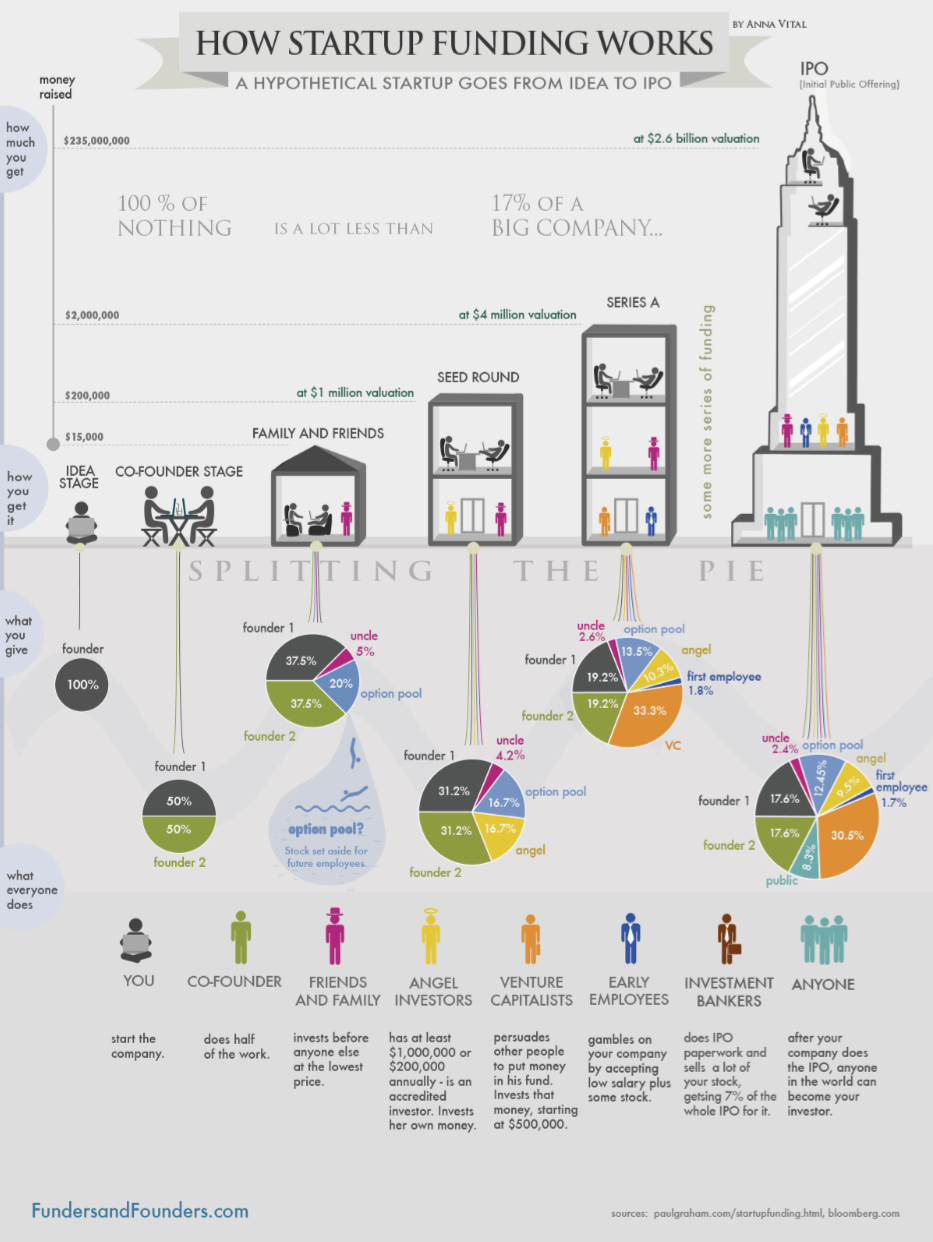

Startups and their highly innovative potential (Bundesregierung 2013, bundesregierung.de) are considered to be of great importance for the economic development in the US, Asia and Europe due to their unimaginable scale effects and enormous valuations as well as their high media attention (Austin, Canipe, Slobin 2015, wsj.com). This paper will provide an overview of means for international startup funding and will examine current changes in startup funding and developments in regards to concern about a new dot-com bubble. -> tl;dr Startups and […]

A few days ago, I received a review copy of Guy Kawasaki ’s latest book, an updated and mostly rewritten version 2.0 of The Art of the Start, his bestselling book from 10 years ago. As most of you know, Guy was an advisor to the Motorola business unit of Google and chief evangelist of Apple and still keeps busy as an executive fellow at the Haas School of Business at U.C. Berkeley and a Venture Capitalist. The 64% longer […]

Do you remember boomf? It’s your instagrams on marshmallows! I came across them last year in June and they seem to be quite popular these days. Just before Valentine’s Day, I spotted them at Selfridges on Oxford Street in London. Basically, they offered a special Valentine’s Day special, allowing you to upload your favourite photos to their system on a local wifi to get them printed on marshmallows, cupcakes or macarons. Also, you could choose from some preselected stock photos if you happen to […]

FFWI wins Neumacher Gründerwettbewerb 2014 – Congrats to FAST FORWARD IMAGING and the entire team. How incredibly cool is that. Even more reasons to try their awesome automatically cropped 360° hi-res product photography solution.

DISCLAIMER: FFWI is a company I am involved with as a managing director.

FAST FORWARD IMAGING is on its way to the start-up competition finals at ‚Neumacher‘ and ‚StartmeupHK‘. The Berlin based hardware startup proceeded to the next round at the startup competitions “Neumacher” and “StartmeupHK” […]

DISCLAIMER: Fast Forward Imaging is a company I am involved in as a managing director.

In case you ever wondered what else you could do with your instragram pictures, this might be right for you. Mint Digital, the London based product development studio who brought you stickigram, is back with boomf. What is it? It’s your instagrams on marshmallows! Why marshmallows and not cakes or something like that? According to Mint Digital: shipping costs. Marshmallows don’t need to be cooled or frozen, they a light and thin so they can be sent via mail not parcel […]

Here are some more impressions from my visit to Google Campus in London. It is a non profit endeavour by Google to provide London with a hub for collaborative innovation in the tech startup scene. It’s located in Shoreditch, opened in 2012 and provides entrepreneurs with speedy wifi, a café, frequent networking and speaking events, a co-working place and access to accelerator programs like seedcamp. With a free permanent resident membership you can gain access 24/7 and hang out at […]