Tag:incubator

While being in Sydney in early 2016, I joined a team to create a food delivery startup as part of a Management & Innovation workshop at UNSW Business School in conjunction with Michael Crouch Innovation Centre. I worked on this project part time while conducting research at UNSW into policy towards entrepreneurship and innovation and drafting a policy review of the Tech Startups Action Plan by the City of Sydney. The workshop was organised around the structure of typical startup accelerator programs, working […]

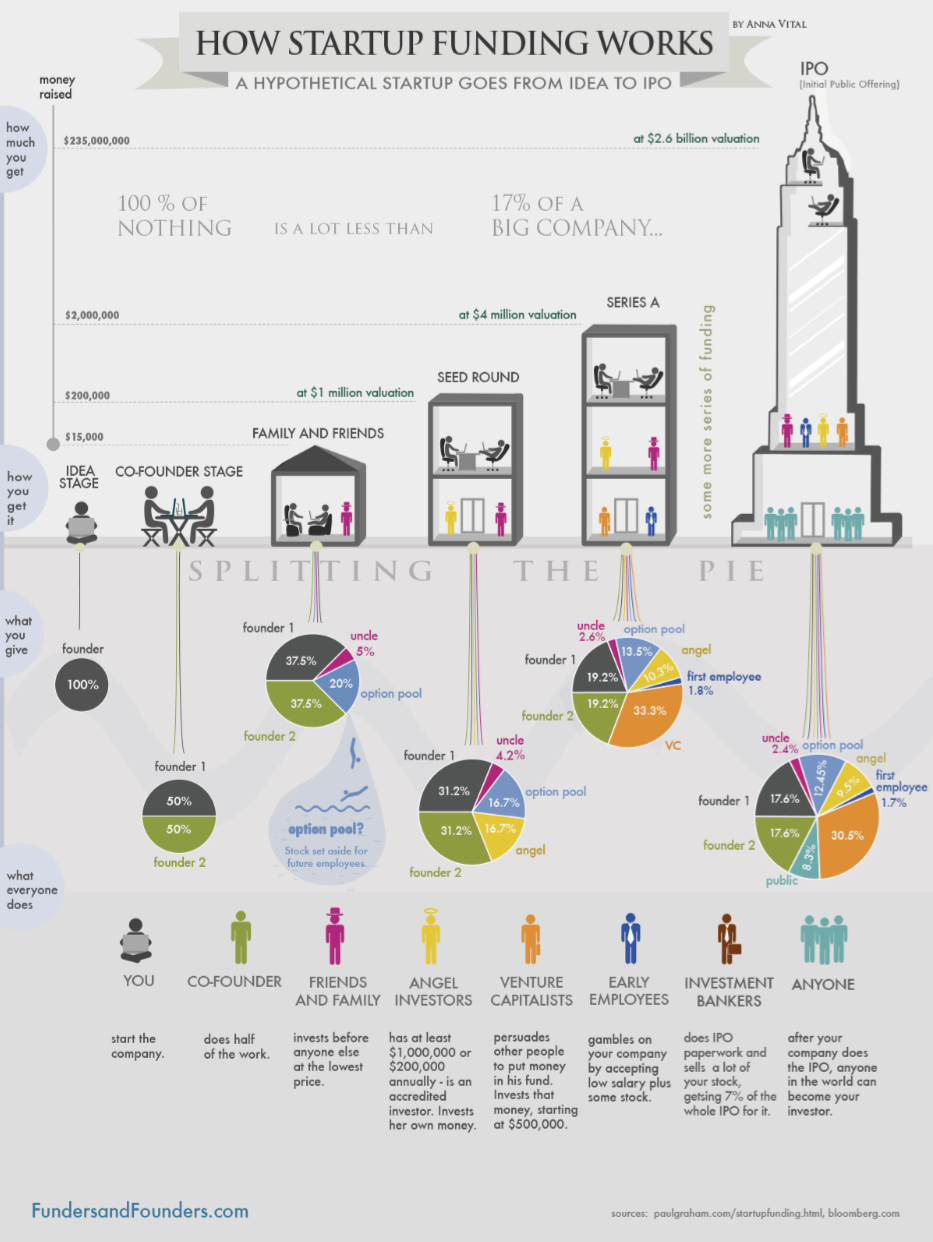

Startups and their highly innovative potential (Bundesregierung 2013, bundesregierung.de) are considered to be of great importance for the economic development in the US, Asia and Europe due to their unimaginable scale effects and enormous valuations as well as their high media attention (Austin, Canipe, Slobin 2015, wsj.com). This paper will provide an overview of means for international startup funding and will examine current changes in startup funding and developments in regards to concern about a new dot-com bubble. -> tl;dr Startups and […]