Tag:exit

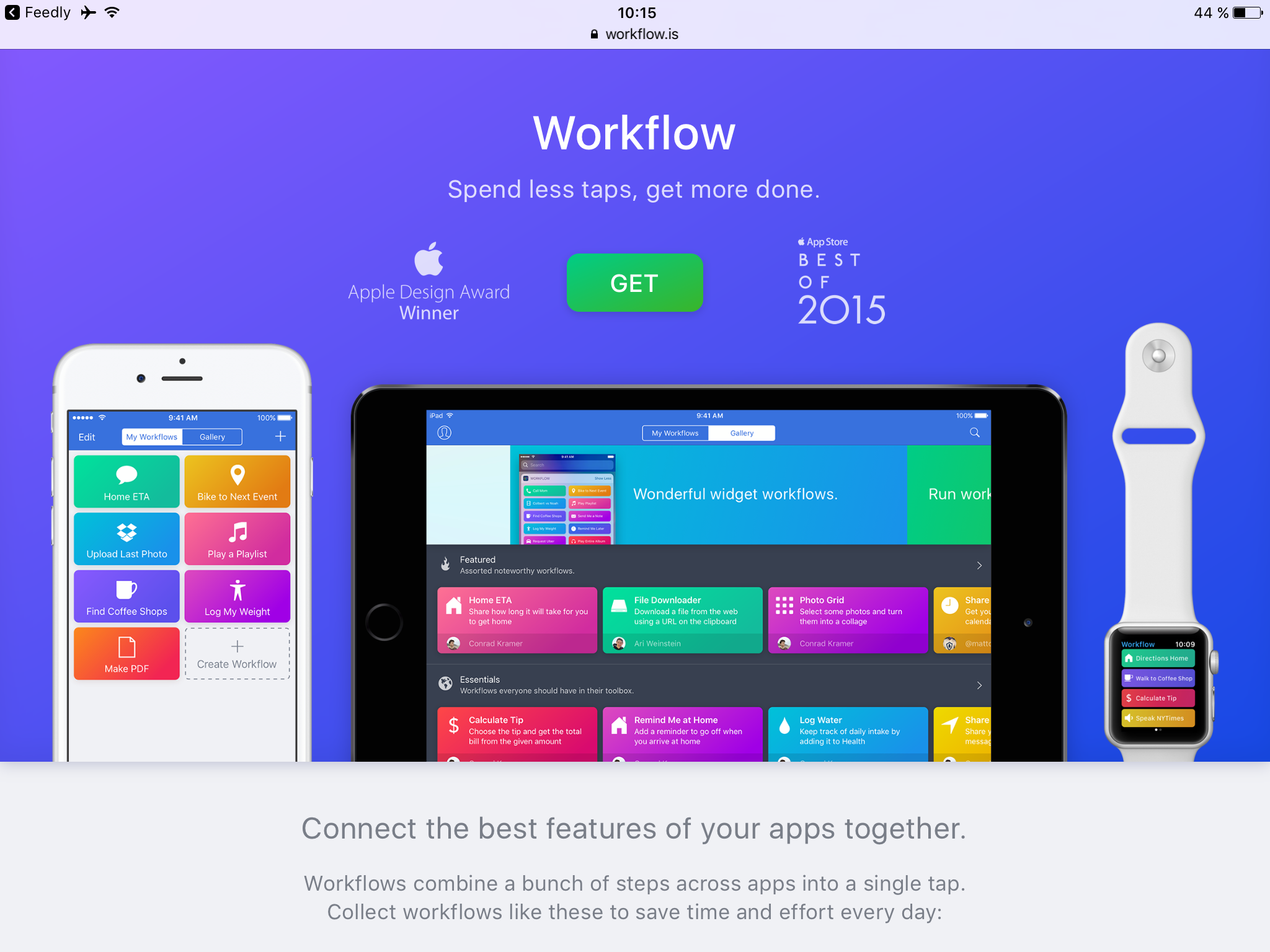

When I was talking about my iPad Pro desktop replacement experiment, I mentioned Workflow, a powerful automation tool I use for tasks of many kinds on the iPad and iPhone. It lets you connect various features of many iOS apps in an easy to use interface that often reminds me of Apple Automator on the Mac, an application that Apple is slowly fading out in my opinion… or at least that is what I thought. As it turned out, Apple […]

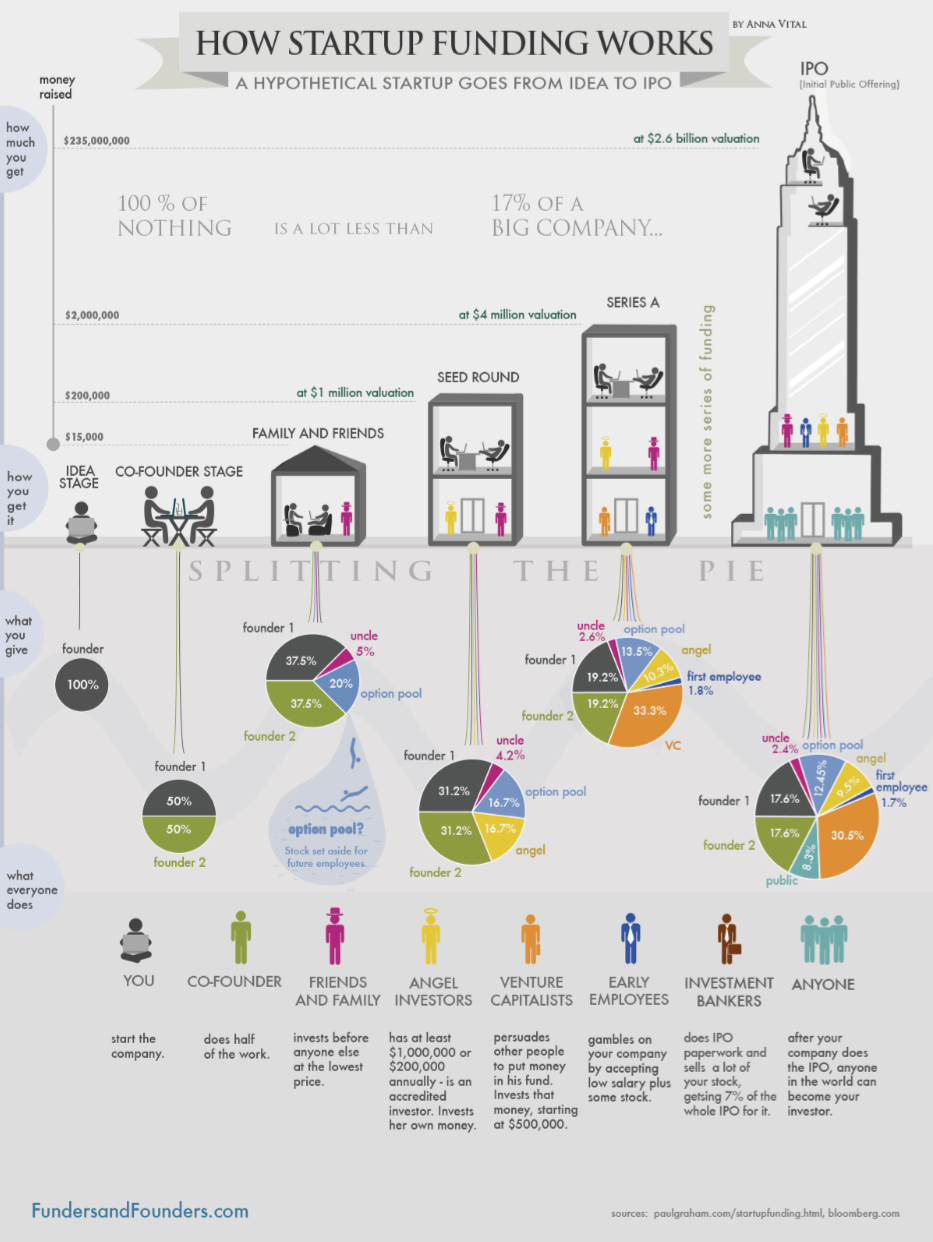

Startups and their highly innovative potential (Bundesregierung 2013, bundesregierung.de) are considered to be of great importance for the economic development in the US, Asia and Europe due to their unimaginable scale effects and enormous valuations as well as their high media attention (Austin, Canipe, Slobin 2015, wsj.com). This paper will provide an overview of means for international startup funding and will examine current changes in startup funding and developments in regards to concern about a new dot-com bubble. -> tl;dr Startups and […]